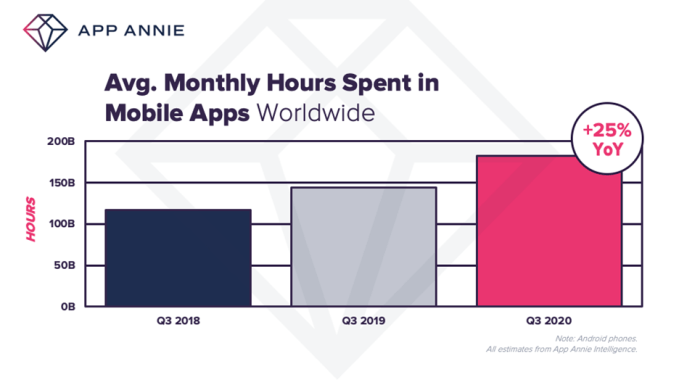

El uso de los teléfonos móviles sigue siendo elevado en medio de la pandemia COVID-19, que ha dado lugar a medidas de distanciamiento social y a políticas de bloqueo, y ha empujado a los consumidores a conectarse en línea para trabajar, estudiar y socializar. Esto, a su vez, ha ayudado a impulsar un gasto récord en aplicaciones durante el trimestre, así como un enorme aumento del tiempo dedicado a las aplicaciones. Según un nuevo informe de App Annie, los consumidores del tercer trimestre descargaron 33.000 millones de nuevas aplicaciones en todo el mundo y gastaron la cifra récord de 28.000 millones de dólares en aplicaciones, lo que supone un aumento del 20% con respecto al año anterior. También pasaron más de 180.000 millones de horas colectivas cada mes de julio, agosto y septiembre de 2020 usando aplicaciones, un aumento del 25% anual.

La empresa de análisis y datos móviles había sugerido anteriormente que la pandemia de COVID-19 tendría un impacto duradero en el comportamiento de los consumidores de telefonía móvil, ya que se adelantó a la misma por lo menos dos o tres años. Esto continuó siendo cierto en el tercer trimestre, con todas las principales tendencias de la telefonía móvil en aumento.

Créditos de la imagen: App Annie

Créditos de la imagen: App Annie

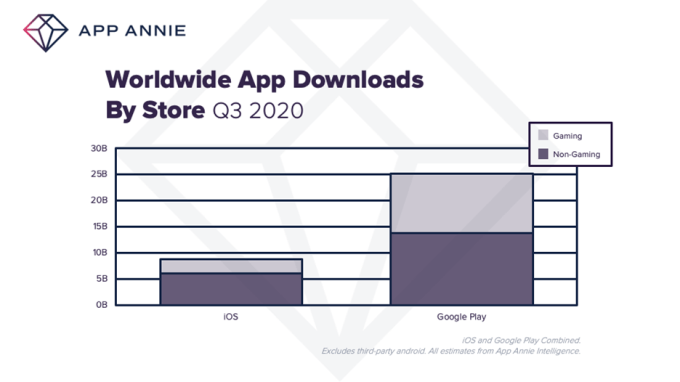

Las descargas de Google Play crecieron un 10% interanual, lo que representa 25.000 millones del total de 33.000 millones de nuevas descargas en el trimestre, mientras que iOS representó casi 9.000 millones de descargas, un 20% más que en el mismo período del año anterior. Las aplicaciones no para juegos de Google Play fueron el 55% de esas descargas, mientras que en iOS la cifra fue un 70% ligeramente superior.

Créditos de la imagen: App Annie

Los principales mercados por descargas fueron India y Brasil en Google Play, mientras que en iOS, los dos primeros siguieron siendo los EE.UU. y China. India, Brasil y México impulsaron el crecimiento en Google Play, mientras que en iOS los impulsores del crecimiento fueron India y Corea del Sur.

Parte del crecimiento de las descargas estuvo directamente relacionado con la pandemia.

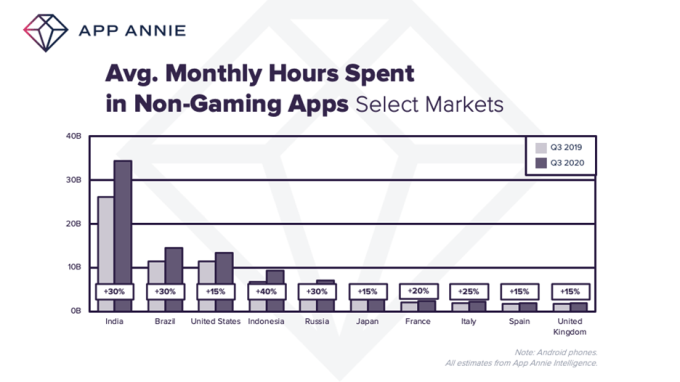

Cuando los estudiantes de México volvieron a la educación a distancia, por ejemplo, las descargas de aplicaciones de educación crecieron un 25% y las de bibliotecas y demostraciones un 270%. Mientras que los consumidores estadounidenses se volcaron al exterior para encontrar actividades en medio de cierres y cierres de negocios, las aplicaciones de Viajes, Navegación y Clima experimentaron un fuerte crecimiento del 50%, 25% y 15%, respectivamente.

En general, Juegos, Herramientas y Entretenimiento impulsaron las descargas de Google Play fuera de la categoría superior, Juegos. Y en iOS Games, la fotografía y el vídeo y el entretenimiento se mantuvieron en las categorías superiores durante cinco trimestres consecutivos.

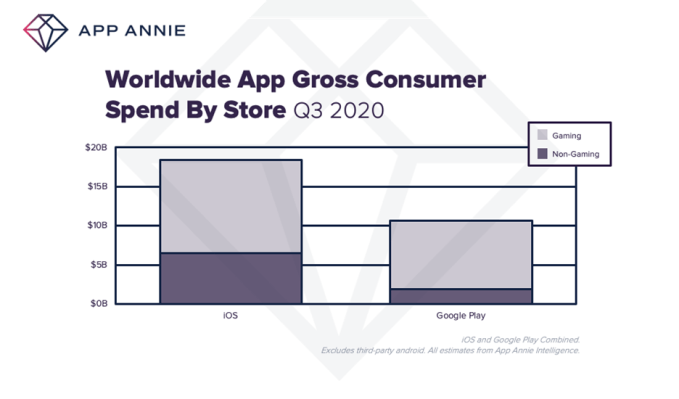

Los consumidores también gastaron un récord de 28.000 millones de dólares en aplicaciones en el tercer trimestre de 2020, el más grande hasta la fecha.

En iOS, el gasto creció un 20% anual hasta alcanzar los 18.000 millones de dólares, mientras que Google Play experimentó un aumento del 35% anual hasta superar los 10.000 millones de dólares. Las aplicaciones no relacionadas con los juegos representaron el 35% de ese gasto en iOS y el 20% en Google Play, en gran parte gracias a las suscripciones.

Créditos de la imagen: App Annie

Los principales mercados para el gasto de los consumidores fueron los Estados Unidos y Japón en ambas tiendas de aplicaciones, con la adición de Corea del Sur para Google Play.

El aumento del gasto de los consumidores en aplicaciones también puede considerarse relacionado con la pandemia y sus impactos. Por ejemplo, los juegos, las actividades sociales y el entretenimiento fueron las categorías más importantes en cuanto al gasto del consumidor en Google Play. Y dentro de la categoría de Entretenimiento, el gasto fue impulsado por las aplicaciones de streaming, como Disney+, Twitch, Globo Play y HBO Max, aplicaciones que podrían haberse beneficiado de que más consumidores se quedaran en casa por motivos de entretenimiento.

En iOS, Juegos, Entretenimiento y Foto y Video fueron las tres categorías principales por el gasto del consumidor. Cuando los deportes volvieron a la televisión en los EE.UU., el gasto en aplicaciones deportivas creció un 55% con respecto al trimestre anterior. TikTok, mientras tanto, se convirtió en la aplicación número 2 por el gasto de los consumidores fuera de los juegos, gracias al aumento de las propinas virtuales para las serpentinas. Sin embargo, el mayor crecimiento trimestral del gasto, fuera de los juegos, fue impulsado por la aplicación de cómics piccoma, YouTube, Tinder y AbemaTV.

Créditos de la imagen: App Annie

Tinder indicó cierta resistencia en el Q3. A pesar de la pandemia, la aplicación subió una posición para llegar al número 1 por el gasto del consumidor. Disney+ también subió un puesto para llegar al No. 4.

En términos de usuarios activos mensualmente, sin embargo, Facebook todavía dominó las listas de éxitos, reclamando las posiciones No. 1 a No. 4 para Facebook, WhatsApp, Messenger e Instagram, respectivamente. Las siguientes aplicaciones más utilizadas fueron Amazon, Twitter, Netflix, Spotify, TikTok y luego Telegram. Esta última entró en el top 10 por primera vez, después de subir dos puestos en el segundo trimestre.

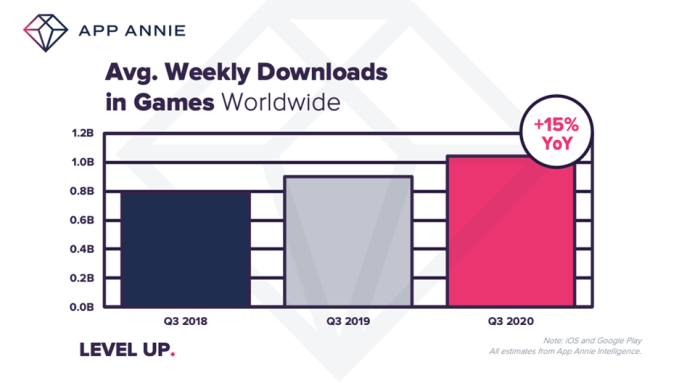

Los juegos también siguen recibiendo un impulso de la pandemia, con descargas semanales que rondan los mil millones por segundo trimestre consecutivo, ya que los consumidores que están bloqueados buscan entretenimiento – un 15% más que en el año anterior.

Créditos de la imagen: App Annie

Los consumidores también gastaron más de 20 mil millones de dólares en juegos en el tercer trimestre, el más grande de la historia. Para finales de año, App Annie pronosticó que los juegos para móviles extenderán su ventaja sobre los juegos de escritorio en 2,8 veces y sobre los juegos de consola en 3,1 veces.

Las descargas de juegos alcanzaron los 14.000 millones en el tercer trimestre, con un aumento del 20% anual en Google Play, hasta alcanzar los 11.000 millones. En iOS, los consumidores descargaron 2.600 millones de juegos. Debido a esto, los juegos representaron una mayor proporción de las descargas totales en Google Play (45%) en comparación con iOS (30%).

Los hallazgos de App Annie siguen el informe Q3 de la empresa de inteligencia de aplicaciones Sensor Tower, publicado a principios de este mes, en el que se observan tendencias similares. Sensor Tower estimó que los ingresos por aplicaciones aumentaron a más de 29.000 millones de dólares en el tercer trimestre, mientras que las descargas de nuevas aplicaciones aumentaron a 36.500 millones.

Sarah Perez